By Zia Saylor

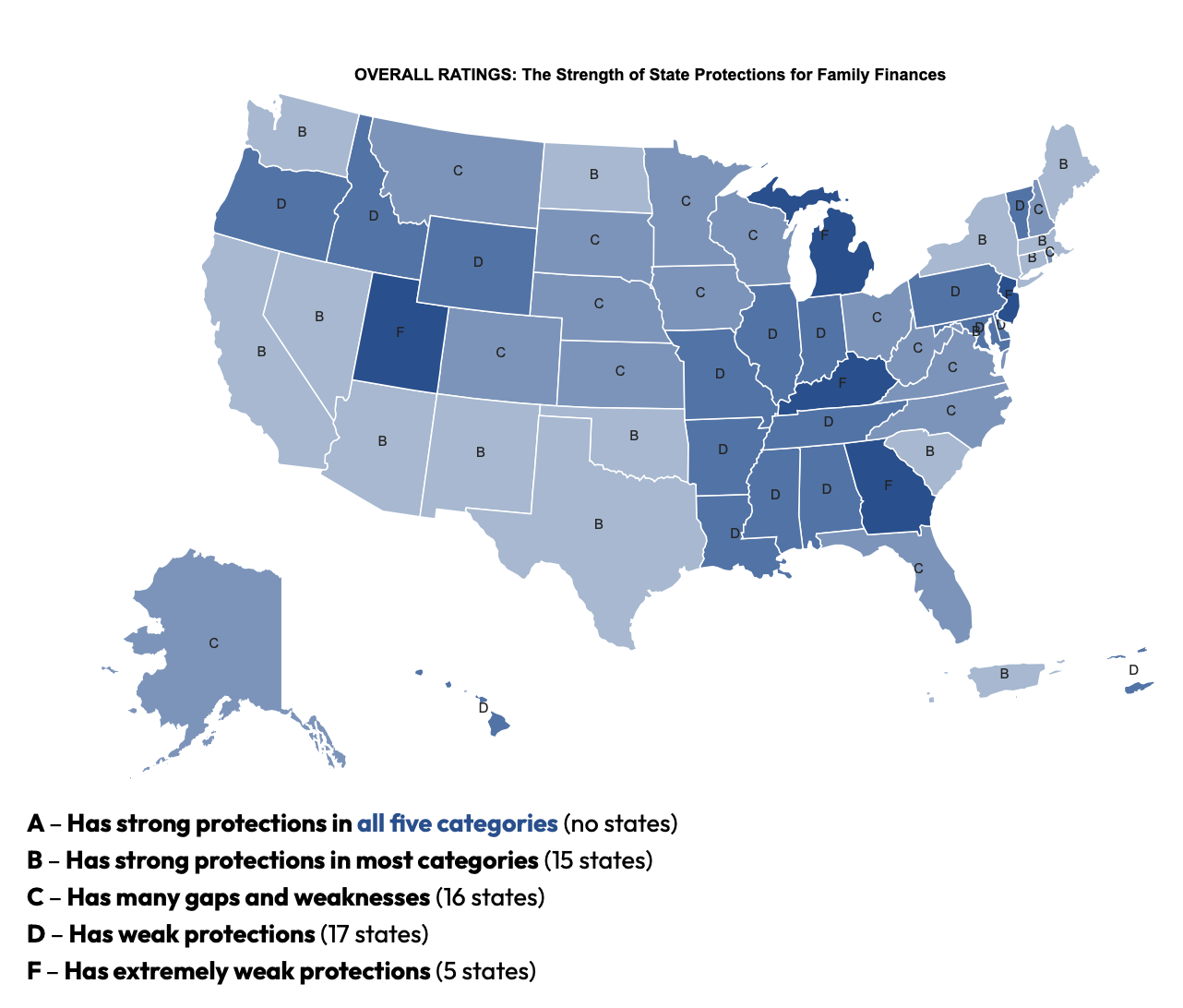

In the recent report released by the National Consumer Law Center (NCLC), Indiana has ranked in the bottom half of states and received a ‘D’ grade for the lack of laws in the state protecting families from being pushed into poverty by debt collectors. For this grading, each state is assessed on five criteria:

-

whether creditors can take so much of their individuals with debt’ wages that the debtor is below the living wage,

-

whether individuals with debt can retain an average-value used car, whether individuals with debt can retain their median-value family home,

-

whether individuals with debt can access baseline funds for essential living costs, and

-

whether creditors can seize and sell debtor’s necessary goods.

A state receiving an “A” would have future-proofing protections to support families in staying above poverty as they pay back their debt. This includes protections such as preventing the debtor (and their family) from relying on wages below the living wage, allowing the debtor to retain their car, house, everyday funds, and necessary goods, without allowing creditors to interfere. These protections are crucial to fostering stable home lives for children and preventing the cycle of poverty.

Graphic Source: National Consumer Law Center

This year, the ratings were particularly disappointing, given that still no state received an “A” by providing all five debtor protections. Given, however, that 15 states got a “B” and another 16 got a “C,” it makes Indiana’s “D” especially bleak, putting it in the bottom half of states. Indiana’s lack of support for families in debt is nothing new: since the start of the report in 2019 when it was awarded a “D-minus,” it has consistently ranked “D.” In fact, from 2019 to 2023, the lowest-ranked categories impacting Indiana’s low grade remained consistent, with the state rated “F” in the home-allowance category for only allowing a home worth 11% of the median state value, and ranked “F” for lack of protection of household goods from seizure and sale.

“We know families in Indiana struggle with debt from necessities like medical bills and utility costs. At the very least, we should ensure that they can keep their heads above water while they are in the repayment process. Indiana’s constitution guarantees individuals who owe money ‘the necessary comforts of life.' Policymakers need to take action to make that promise a reality,” said Director of Indiana Community Action Poverty Institute Erin Macey.

It’s not just inaction at the core of this policy problem: it’s dismissal. Several bills in Indiana in the 2023 legislative session actually would have exacerbated this crisis, indicating that legislative priorities align more with creditors and perpetuating cycles of debt than with the financial empowerment of families. Indiana has already received a “D” for four years in a row. Let’s not make it a fifth year in 2024, and use this coming legislative session to protect Hoosiers from predatory finances and cycles of debt.

Take Action: Send a copy of this report to your state legislators and ask them how they plan to improve Indiana’s grade in the 2024 session or sign up for Hoosiers for Responsible Lending’s action alerts to be notified of opportunities to engage.