Payday Lending: A Drain on Hoosier Families and Communities

|

In 2002, the Indiana General Assembly granted payday lenders an exemption to Indiana's interest rate cap of 36 percent and criminal loansharking limit of 72% APR. In just two decades, payday lenders have established a significant footprint across our state. In 2002, the Indiana General Assembly granted payday lenders an exemption to Indiana's interest rate cap of 36 percent and criminal loansharking limit of 72% APR. In just two decades, payday lenders have established a significant footprint across our state.

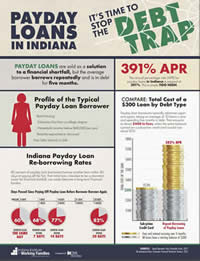

This update on our 2019 report shows that payday lenders drain over $29 million in finance charges from Hoosier borrowers annually on loans that average $386. Effective January 2023, the maximum payday loan increased from $605 to $715, and lenders can charge rates as high as 391% Annual Percentage Rate (APR). As the report shows, Indiana saw a precipitous drop in loan volume during 2020, likely due to robust federal support in response to the COVID-19 pandemic. Since the expiration of important federal supports such as the expanded Child Tax Credit, additional unemployment insurance, and rental assistance, payday loan volumes are trending toward their pre-pandemic levels.

|

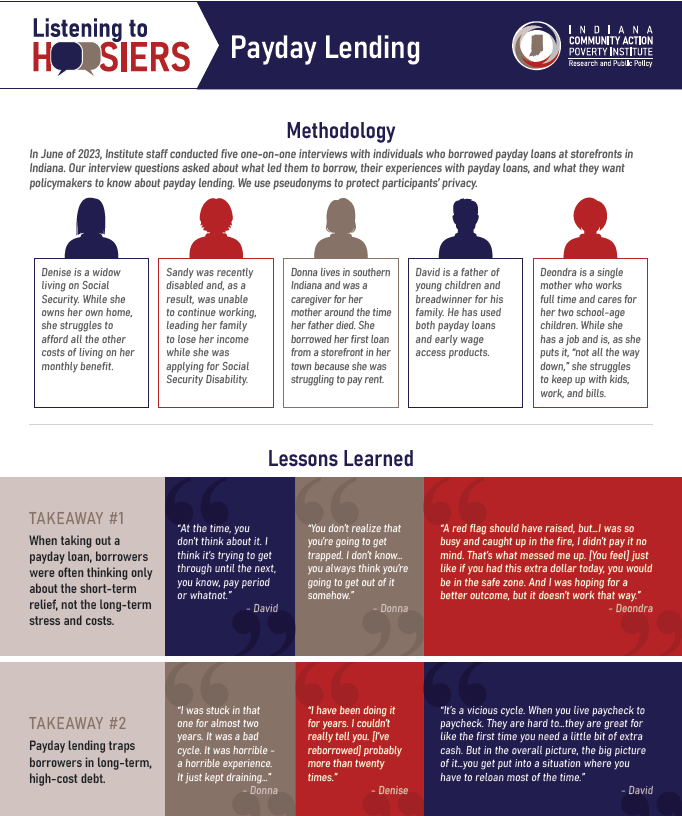

Listening to Hoosiers: Payday Lending

|

Payday loans are short-term, extremely high-cost loans that trap borrowers in costly debt. Our interviews with Hoosiers add to the existing understanding of who borrows payday loans and why, what they know (and don't know) when they borrow, how the cycle of borrowing and reborrowing affects them, and what supports they would like to see instead.

|

2019 Financial Drain Report

Our 2019 report, Financial Drain: Payday Lenders Extract Millions from Hoosier Communities, documents the scope and impact of these lenders on families and communities, finding:

- Payday lenders have drained over $300 million in finance charges from Hoosier families and communities in the past five years.

- There are 262 payday loan storefronts across Indiana, and out-of-state companies operate 86% of them.

- Payday storefronts are disproportionately located in low-income communities and communities of color.

- The typical payday loan borrower has a median income of just over $19,000 per year and re-borrows eight to ten times, paying more in fees than the amount originally borrowed.

- Many borrowers experience a cascade of negative consequences, include overdrafts, defaults, involuntary bank account closure, bankruptcy, and more.

Quick Facts About Payday Lending Quick Facts About Payday Lending

Payday loans trap borrowers in a cycle of high-cost debt. Learn the facts:

- The typical borrower is a renter earning less than $40,000 per year.

- 60% of payday loans are re-borrowed the same day an old loan is repaid.

- Compared to carry a balance on a credit card, a payday loan can cost 15-20 times as much.

- Payday lending can drive borrowers into bankruptcy.

- Indiana has one of the highest bankruptcy rates in the country.

- Payday lenders drain tens of millions in fees each year from Indiana's economy.

Polling Shows Hoosiers Support Reform Polling Shows Hoosiers Support Reform

Bellwether Research & Consulting asked 600 Hoosiers about payday lending:

- Nearly 90% of Hoosier voters support a 36% APR cap, even after hearing pro-industry arguments against the proposal.

- Eight-seven percent say payday loans are a "financial burden" and 84% think they are "harmful."

- Three out of four voters would oppose a new payday loan store opening in their neighborhood.

- More than one third of polling respondents had taken out or knew someone who had taken out a payday loan.; these respondents expressed similarly high levels of support for reform.

- A large & diverse coalition also supports payday lending reform in Indiana.

Other Resources Related to Payday and Subprime Lending

|